In the global financial market, U.S. Treasury bonds have long been regarded as the benchmark for risk-free assets. However, a stark reality is eroding this long-held belief: although the U.S. government has never formally missed a payment, a more insidious phenomenon of "soft default" has quietly emerged.

For investors holding long-term U.S. Treasuries (especially 20- and 30-year bonds), persistent inflation is continuously devouring their nominal interest, causing real yields to linger in negative territory for extended periods. This means that from a purchasing power perspective, the capital invested today will not be able to buy the same amount of goods and services when it is returned in the future.

For overseas investors, particularly central banks of major creditor nations like China and Japan, the losses are twofold. In addition to the direct erosion from inflation, the long-term depreciation trend of the U.S. dollar further diminishes the real value of these dollar-denominated assets. Allocating foreign exchange reserves to U.S. Treasury bonds is gradually turning into a slow but certain drain on wealth.

This method of defaulting in substance by devaluing the currency, while not triggering a technical debt crisis, fundamentally shakes long-term global confidence in the credit of the U.S. dollar and the financial system behind it. When the traditional safe haven is no longer safe, global capital will inevitably begin to seek a new anchor of value. A profound era of global asset reallocation may have already begun.

The Snowballing Debt: U.S. National Debt and Interest Payments

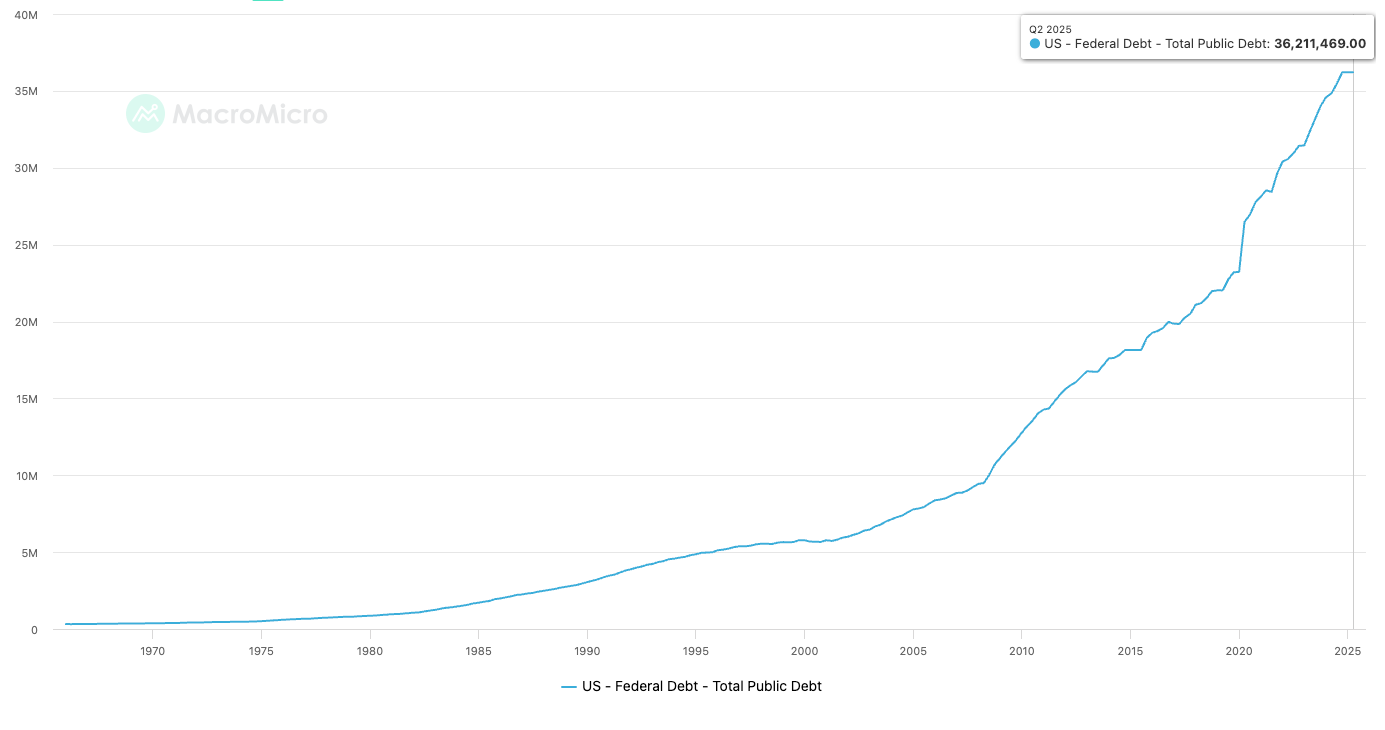

The scale of U.S. national debt has reached a historic and unsettling magnitude. As of 2025, the total national debt of the United States has surged to an astonishing level exceeding $37 trillion. This figure not only far surpasses its annual Gross Domestic Product (GDP) but is also equivalent to a debt of over $4,600 for every person on Earth.

This colossal number is not static; it continues to grow at a rate of billions of dollars per day. The interest payments required to service this massive debt have evolved into a heavy and ever-increasing fiscal burden. In the 2025 fiscal year, the net interest payments on U.S. national debt are projected to exceed $1 trillion.

This enormous expenditure has already surpassed the budgets for critical sectors such as defense, education, and healthcare, becoming one of the fastest-growing parts of the U.S. federal budget. This means that a progressively larger portion of the taxes contributed by American taxpayers is not being used to improve public services or invest in infrastructure, but is flowing directly into the pockets of bondholders. This has created a vicious cycle of "borrowing new money to pay off old debts" while paying exorbitant interest.

This snowball effect of debt not only squeezes future fiscal space but also forces the government to continually rely on monetary expansion to dilute the debt, posing a potential threat to global financial stability.

How Central Banks Use Inflation to Reduce Debt

When a nation's debt becomes excessively large, governments and central banks have a more subtle and frequently used tool at their disposal, beyond traditional methods like raising revenue (increasing taxes), cutting spending, or outright default. That tool is inflation.

The core logic of this strategy is that most government debt is denominated in a fixed amount of its own currency. By engineering inflation, a central bank can decrease the real purchasing power of that currency, thereby cleverly and gradually reducing the true value of the debt it owes.

This process is typically initiated by the central bank through expansionary monetary policy. For instance, the central bank might lower interest rates to encourage borrowing and spending, or more directly, it might purchase government bonds on a massive scale through operations like Quantitative Easing (QE). When a central bank effectively "prints money" to buy government bonds, it is financing the government's deficit spending.

This injects a large amount of new liquidity into the economic system. When the growth in the money supply outpaces the growth in the production of goods and services, prices generally rise, leading to inflation.

For the government, the nominal amount of principal and interest it repays does not change. However, due to inflation, the real value of that money has been discounted. For example, if a government borrowed $10 billion ten years ago and the cumulative inflation rate over that decade was 50%, the $10 billion it repays today would only have the purchasing power equivalent to about $6.67 billion at the time the loan was made.

For the investors holding these bonds—whether they are domestic pension funds, banks, or foreign central banks—while they receive the full nominal value of their investment, its real purchasing power has been significantly diminished.

U.S. Treasuries and Gold: An Eternal Financial Game

U.S. Treasuries and gold are both regarded as important safe-haven assets in the global financial system, yet their relationship is complex, subtle, and often exhibits a "seesaw" effect of mutual counterbalance.

In traditional finance, U.S. Treasuries are considered the world's safest asset, backed by the full faith and credit of the U.S. government. Gold, on the other hand, is an ancient store of value spanning millennia. It generates no interest (it is a "zero-yield asset"), and its value derives from its physical scarcity, chemical stability, and a universal consensus that it is the ultimate "insurance" against inflation and geopolitical crises. The key determinant of their relationship is the real yield on U.S. Treasuries, which is the nominal yield minus the rate of inflation.

When Real Yields Are Positive and Rising: When the real yield is positive and increasing, it means the return from holding U.S. Treasuries outpaces inflation, offering investors a risk-free growth in real purchasing power. In this environment, holding gold, which yields nothing, becomes less sensible. The opportunity cost of holding gold rises significantly; for every ounce of gold held, an investor forgoes the stable, positive real return offered by U.S. Treasuries. Consequently, capital tends to flow from the gold market to the bond market, putting downward pressure on the price of gold.

When Real Yields Are Negative or Falling: This is the backdrop for our discussion of a "de facto default." If the inflation rate is higher than the nominal interest rate on Treasury bonds, holding these bonds to maturity will actually result in a loss of purchasing power. At this point, the appeal of U.S. Treasuries as a "risk-free asset" is severely diminished. The disadvantage of gold as a non-interest-bearing asset is completely offset, and its attributes as a store of value and a hedge against currency devaluation come to the forefront. Holding U.S. Treasuries means "steadily losing money" in real terms, while gold offers the possibility of preserving value. Therefore, capital will flow out of fixed-income assets like Treasuries and seek refuge in gold, driving its price higher.

When the market grows concerned about a government's ability to repay its debt or the long-term purchasing power of its currency, the credit foundation of its bonds begins to shake. This is when gold's role as an "external hedge" to the fiat currency system becomes apparent. It is unaffected by the credit risk of any single nation, making it the ultimate safe haven to hedge against sovereign debt risk and currency depreciation.

In the current context of high U.S. government debt and persistent long-term inflationary pressures—the "de facto default" scenario—the scales are tipping significantly in favor of gold. When the safest bond asset can no longer provide a safe, real return, the instinctive drive of capital to preserve its value will inevitably lead it to gold.

Bitcoin: The "Gold" of the Digital Age and a Trustless Asset

In the discussion of capital outflows triggered by the "de facto default" of U.S. debt, the role of Bitcoin has become increasingly prominent. It is not just a synonym for cryptocurrency but an emerging macro asset with unique properties. To understand Bitcoin's strategic position in the current financial landscape, it is crucial to analyze its core asset attributes. These attributes, especially their striking similarities to gold, are the fundamental reason why the market has hailed it as "Digital Gold."

Absolute Scarcity is the most fundamental commonality between Bitcoin and gold. Bitcoin's total supply is permanently locked at 21 million coins by its underlying protocol and can never be increased. This stands in stark contrast to fiat currencies, which can be printed infinitely by central banks. While gold's scarcity stems from physical limitations in the Earth's crust and the difficulty of mining, Bitcoin achieves absolute scarcity through mathematical algorithms. Its supply growth path is completely transparent and predictable, with its issuance rate halving approximately every four years, continuously slowing its growth.

From an economic perspective, the Proof-of-Work (PoW) mechanism endows Bitcoin with a production cost. It transforms two real-world inputs, computing power (hash rate) and electricity, into a form of abstract "digital labor." It is this process—requiring the continuous consumption of real-world resources to "mint" new coins—that gives its value a solid cost basis.

Bitcoin's architecture fundamentally subverts financial control. Its network is not owned or operated by a single entity but is collectively maintained by a global, voluntary coalition of tens of thousands of independent nodes. This distributed structure eliminates the possibility of unilateral control by a central authority (like a government or bank), making actions such as freezing accounts, confiscating funds, or censoring transactions technically infeasible. It is this "trustless" characteristic—requiring trust only in mathematics and code, not in intermediaries—that shapes Bitcoin into a truly sovereignly independent asset. It exists outside the traditional financial and political systems, providing an ultimate safe haven for wealth.

At the same time, Bitcoin retains the scarcity of gold while completely shedding the constraints of its physical form. Its divisibility, transferability, and portability allow it to be finely divided to suit any transaction size and to compress immense wealth into intangible digital information, enabling near-instantaneous, low-cost global transfers via the internet. This extreme portability and liquidity represent a fundamental advantage that physical gold cannot match.

An Indispensable Strategic Asset in an Era of Credit Dilution

When traditional "risk-free assets" can no longer provide a safe, real return due to persistent inflation and currency debasement, the flood of capital will inevitably seek new anchors of value. In this historic shift, Bitcoin, with its unique digital attributes, is evolving from a fringe speculative item into an indispensable strategic component of modern investment portfolios.

For individual investors, Bitcoin's status has undergone a fundamental leap—from being a mere "lottery ticket" for high-risk, high-return bets to becoming a core asset for defending personal wealth and seeking long-term growth. Faced with ongoing inflationary pressures in major global economies and the constantly diluted purchasing power of fiat currencies, Bitcoin offers mathematical certainty with its programmed, absolute scarcity capped at 21 million coins. Individuals are increasingly allocating a portion of their savings to Bitcoin, viewing it as a digital form of "hard asset" to preserve their hard-earned wealth and hedge against the inevitable risk of fiat currency devaluation.

Furthermore, the maturation of financial instruments has significantly lowered the barrier to entry. The approval of spot Bitcoin ETFs in multiple jurisdictions since 2024 allows ordinary investors to conveniently and compliantly hold Bitcoin through traditional brokerage accounts, without having to worry about technical challenges like private key management.

If you do not prefer ETFs, individuals can still achieve absolute control over their assets through self-custody, free from the interference of any third-party institution. In today's world of increasing financial system risks, this holds an unparalleled appeal for individuals who prioritize asset security and privacy.

For institutional investors, Bitcoin represents a new cornerstone for diversification, liquidity, and risk hedging. Institutional adoption is the most significant catalyst elevating Bitcoin's status. Pension funds, endowments, insurance companies, and corporate treasuries that once dismissed crypto assets are now incorporating them onto their balance sheets with an increasingly open and prudent approach.

The core driver is its outstanding performance as a portfolio diversification tool. Historical data has shown that Bitcoin's price movements have a very low correlation with mainstream asset classes like stocks and bonds. This means that adding a small allocation of Bitcoin to a portfolio can effectively improve risk-adjusted returns without significantly increasing overall risk. Its hedging effect is particularly pronounced in market environments where both stocks and bonds are declining simultaneously.

The success of spot Bitcoin ETFs has been the "icebreaker" for institutional entry. It not only solved the three core obstacles of compliance, custody, and liquidity but also marked the official birth of Bitcoin as a mainstream, regulated, and investable asset class. According to data from top asset management firms like BlackRock, the scale of capital flowing into Bitcoin ETFs has remained substantial throughout 2025, reflecting that institutional capital is steadily and continuously increasing its exposure through these regulated channels. According to data from CoinGlass, the total assets under management (AUM) for spot Bitcoin ETFs have already surpassed $150 billion.

Furthermore, as the global regulatory framework becomes clearer, the compliance pathways for institutional Bitcoin allocation are becoming more defined. From the European Union's MiCA (Markets in Crypto-Assets) legislation to potentially more comprehensive digital asset regulations in the United States, regulatory certainty is replacing the ambiguity of the past. This provides the confidence and legal foundation needed for the investment committees of large institutions.

Today, institutions view Bitcoin as a highly liquid "digital commodity" or a "non-sovereign store of value," positioning it alongside gold as a macro-hedging tool, but one with greater elasticity for growth.