This report aims to provide an in-depth analysis of the increasingly complex relationship between United States Treasury securities (US Treasuries) and gold. The core argument of this report is that while the traditional negative correlation between gold and US real yields remains valid under certain market conditions, a more powerful and structural new dynamic is gradually taking precedence. The root of this shift lies in the "de facto default" of US sovereignty. This concept does not refer to a technical failure to pay, but rather to a systemic and profound erosion of market confidence in America's fiscal sustainability and political stability, marked by the historic first-time downgrade of US sovereign credit rating by all three major credit rating agencies. This loss of confidence is triggering a structural shift in global capital allocation. In this context, gold's role is no longer merely that of an alternative to US Treasuries based on opportunity cost; it is now being actively used as the ultimate hedge against the risks of the "risk-free asset" itself.

America's Fiscal Predicament: An Unprecedented Debt Burden

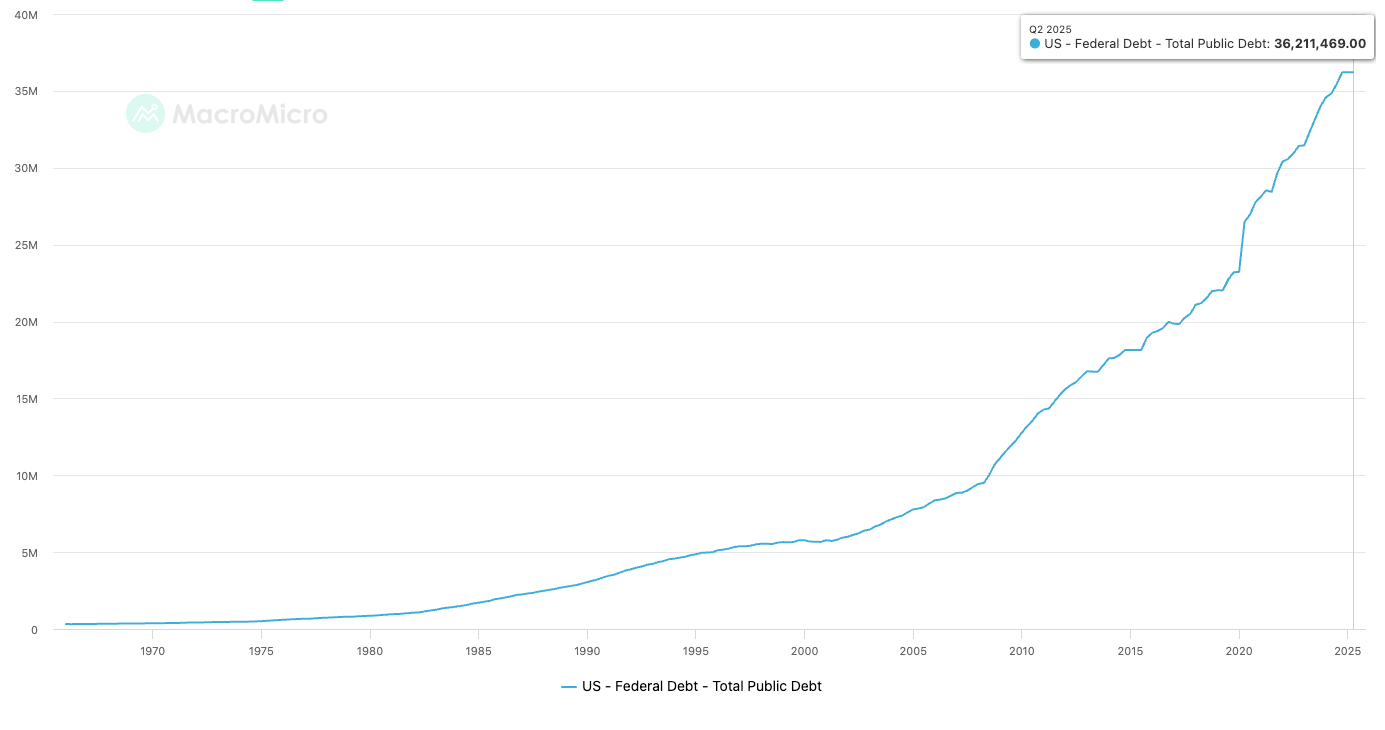

The total amount of US national debt has climbed to an astonishing level. As of the end of 2025, the total US national debt has reached approximately $37.94 trillion. According to projections from the Congressional Budget Office (CBO), if current policies remain unchanged, this figure will exceed $52 trillion by the end of fiscal year 2035. Such a massive scale of debt, when distributed among every US citizen, amounts to a liability of over $111,000 per person. This enormous nominal value signifies that the US government has a huge and persistent financing need from global capital markets.

The debt-to-GDP ratio is a core indicator for assessing a nation's ability to repay its debts. As of fiscal year 2025, the US debt-to-GDP ratio has reached as high as approximately 125%. This ratio hit a historic high of 133% during the peak of the COVID-19 pandemic in the second quarter of 2020. In sharp contrast, the credit rating agency Moody's has pointed out that the average debt-to-GDP ratio for AAA-rated sovereign nations is far below the current US level, highlighting the relative fragility of America's fiscal situation. Moody's further predicts that by 2035, the federal debt burden will climb to around 134% of GDP.

Soaring Debt Service Costs: The Debt Spiral Dynamic

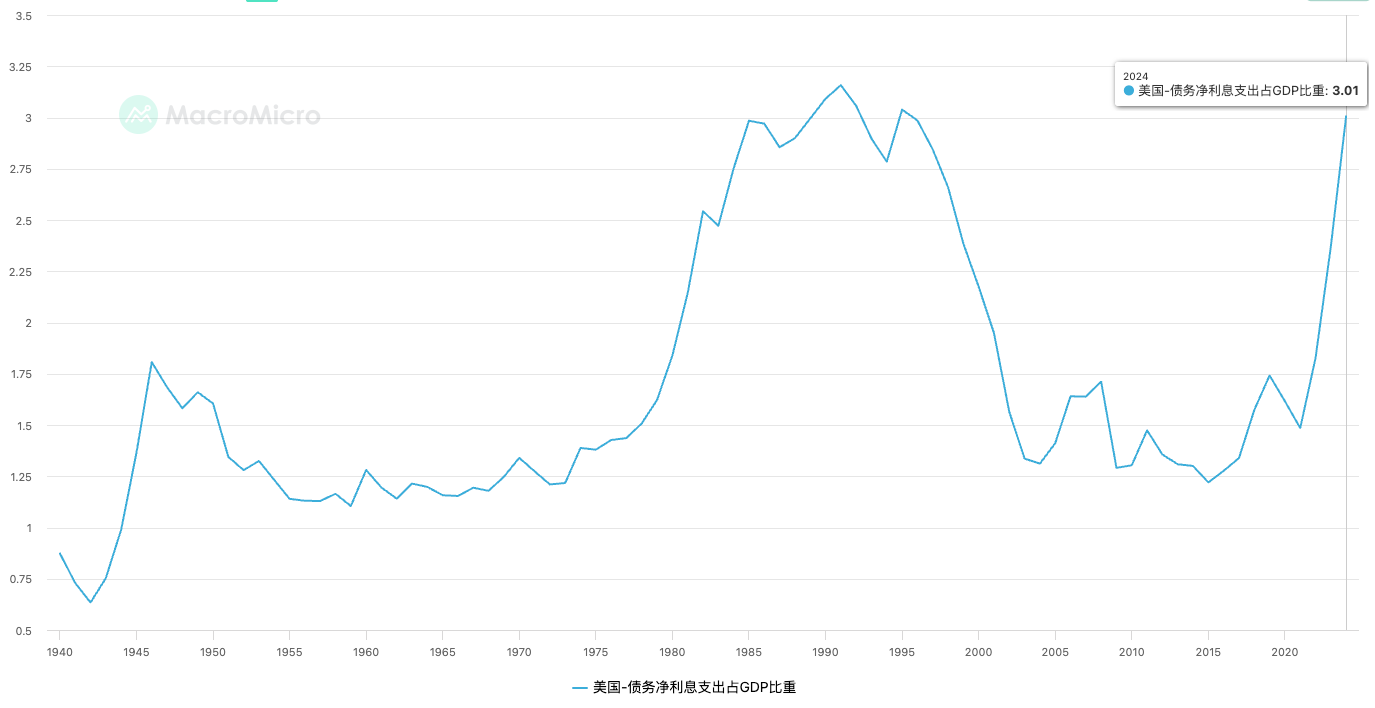

As the debt base expands and interest rate levels rise, interest expense has become the fastest-growing part of the US federal budget. In fiscal year 2024, the federal government's net interest payments reached a high of $879.9 billion, accounting for 13% of all expenditures for the year, a scale that has already surpassed spending on Medicare or national defense. Currently, the average interest rate on US national debt is 3.36%, which means the daily interest cost exceeds $2.6 billion.

Underlying this phenomenon is a dangerous fiscal feedback loop known as the "debt spiral." The monetary tightening cycle initiated by the Federal Reserve to combat inflation has directly pushed up the government's financing costs. Higher interest rates dramatically increase the cost of refinancing existing massive debts and paying interest on them. Moody's explicitly stated in its rating report that it expects federal interest payments to consume approximately 30% of government revenue by 2035, a significant increase from just 18% in 2024. This vicious cycle, where higher interest rates lead to higher interest payments, which in turn result in larger fiscal deficits that compel the government to issue more new debt, creates a self-reinforcing dynamic. This deteriorating situation indicates that America's fiscal condition has become exceptionally sensitive to interest rate policy, and actions taken by the central bank to maintain price stability may inadvertently exacerbate the government's fiscal instability.

For the first time in history, the United States has simultaneously lost the highest sovereign credit ratings (AAA/Aaa) from all three major international credit rating agencies: Standard & Poor's (S&P), Moody's, and Fitch. This series of rating downgrades serves as an authoritative confirmation of the fundamental erosion of US creditworthiness in the market. The rationales provided by the three agencies for the downgrades are highly consistent, all pointing to several core issues: an unsustainable debt trajectory, ballooning interest costs, and, crucially, the deterioration of governance and decline in political stability. The repeated debt ceiling standoffs were specifically mentioned, indicating that the market's assessment of US sovereign risk is no longer confined to purely economic dimensions but is now deeply intertwined with political risk. This shift means that the foundational status of US Treasuries as the global "risk-free asset" is being eroded, and their pricing is beginning to incorporate a non-negligible governance risk premium.

The Fundamental Relationship Between US Treasuries and Gold: Real Yield, Opportunity Cost, and the US Dollar

The Primacy of Real Interest Rates

The key to understanding the relationship between gold and US Treasuries lies in distinguishing between nominal and real yields. The core variable driving their relationship is not the nominal yield shown on the face of a Treasury bond, but the real yield after adjusting for inflation expectations (Real Yield = Nominal Yield - Inflation Expectation). As of August 2025, the annual US inflation rate (CPI) was 2.9%, with core inflation at 3.1%. During the same period, the nominal yield on the benchmark 10-year US Treasury note fluctuated around 4%. Based on this, it can be estimated that the 10-year real yield at the time was approximately 4% - 2.9% = 1.1%. A positive real yield means the purchasing power of an investor's assets is growing, while a negative real yield means it is being eroded by inflation.

Opportunity Cost: The Core Mechanism of Negative Correlation

Gold is a non-yielding asset; it does not generate any interest or dividend income. Therefore, holding gold incurs an opportunity cost, which is the return an investor forgoes by not holding other interest-bearing assets (like US Treasuries).

When real yields rise: The return on interest-bearing assets like US Treasuries becomes more attractive. This increases the opportunity cost of holding gold, leading investors to sell gold and buy bonds instead. Demand for gold decreases, putting downward pressure on its price.

When real yields fall: Especially when real yields drop into the zero or negative territory, the return on holding bonds becomes negligible and may not even offset inflation, meaning holding bonds guarantees a real loss of purchasing power. At this point, the opportunity cost of holding gold drastically decreases or even disappears. Compared to bonds that guarantee a loss, non-interest-bearing gold becomes highly attractive as a store of value, prompting investors to increase their allocation to gold, thereby pushing up its price.

The Dual Role of the US Dollar

The US dollar plays a complex and critical dual role in the relationship between gold and US Treasuries, acting as both the unit of account and a competing safe-haven asset.

As the sole pricing currency for gold globally, the strength of the dollar directly impacts the price of gold. When the dollar weakens relative to other currencies, it becomes cheaper for investors holding non-dollar currencies to buy gold, which stimulates global demand and pushes up the price of gold in US dollar terms. Conversely, a strong dollar suppresses demand for gold, putting pressure on its price. This constitutes the typical negative correlation between the dollar and the price of gold.

The dollar itself, as the world's primary reserve currency and safe-haven asset, competes with gold. In certain moments of global crisis, market panic can drive investors to flock to what are perceived as the two safest assets simultaneously: gold and the dollar. In this "co-flight to safety" scenario, their traditional negative correlation may temporarily break down, with both assets rising in tandem. However, a long-term examination of historical data reveals a potential contradiction. Although the opportunity cost model has been strongly supported by empirical evidence during specific periods, other studies point out that over a longer time horizon, this relationship is "uncertain and unstable," with some even arguing that no stable correlation exists between the two. This is not a contradiction in the data itself, but rather reveals the inherent complexity of the relationship. It suggests that while real yield and opportunity cost are the dominant drivers, they are not the only factors. Under certain conditions, the influence of other factors such as safe-haven demand, geopolitical risk, and inflation hedging can rise sharply, even overshadowing the dominant role of real yields. Therefore, the key question is not whether the relationship exists, but under what circumstances and why the primary driver (real yield) is overridden by secondary drivers (like fear and systemic risk).

De Facto Default: When the "Risk-Free Asset" Becomes the Risk Itself

According to the standard definition, a sovereign default occurs when a national government fails or refuses to repay its debt in full upon maturity. However, such a default can be undeclared and may be triggered by non-economic factors like political turmoil. A "de facto" state refers to a situation that exists in reality, even if not legally recognized.

The de facto default mentioned here does not refer to a technical payment failure event, but rather to a market state. In this state, global market participants begin to treat a nation's sovereign debt as if its "risk-free" credit guarantee is no longer reliable. This state is triggered by a severe and persistent loss of confidence in the government's political will and fiscal capacity to meet its long-term debt obligations, even if it is still making its current payments on time. The unprecedented and unanimous downgrades by the three major rating agencies are the most compelling evidence that the United States has entered such a "de facto default" state.

The 2011 Debt Ceiling Crisis and the S&P Downgrade

The events of 2011 provide a perfect case study of how a crisis of confidence in America's governance capabilities can fundamentally alter the behavior patterns of various asset classes. The 2011 crisis stemmed from an intense political standoff. After the 2010 midterm elections, the Republican Party gained control of the House of Representatives and insisted that any increase in the debt ceiling must be accompanied by massive fiscal spending cuts. This led to a months-long political impasse between the Democratic-controlled Senate and the Obama administration and the House. As the Treasury Department's projected "X-date"—the day when all borrowing authority and extraordinary measures would be exhausted—of August 2, 2011, drew nearer, market fears of a potential technical default by the US surged. Although Congress passed the Budget Control Act of 2011 at the last minute on August 2, raising the debt ceiling and setting future deficit reduction targets, the protracted political battle had already inflicted irreversible damage on market confidence.

The climax of the crisis occurred on August 5, 2011, when Standard & Poor's announced it was lowering the long-term sovereign credit rating of the United States from AAA to AA+. In its official statement, S&P explicitly noted that the downgrade was not due to a lack of capacity to repay debt, but was based on two core judgments: an insufficient fiscal consolidation plan and political risk.

Insufficient Fiscal Consolidation Plan: S&P believed that the just-passed Budget Control Act "fell short of what, in our view, would be necessary to stabilize the government's medium-term debt dynamics."

Political Risk: More critically, S&P concluded that "the effectiveness, stability, and predictability of American policymaking and political institutions have weakened" at a time of ongoing fiscal and economic challenges.

S&P's wording directly corroborates the "de facto default" argument: the core issue was not economics, but the institutional vulnerability exposed by governance failure and political gridlock. The downgrade event, however, triggered a violent and seemingly contradictory market reaction, profoundly revealing the inherent hierarchy of safe-haven assets.

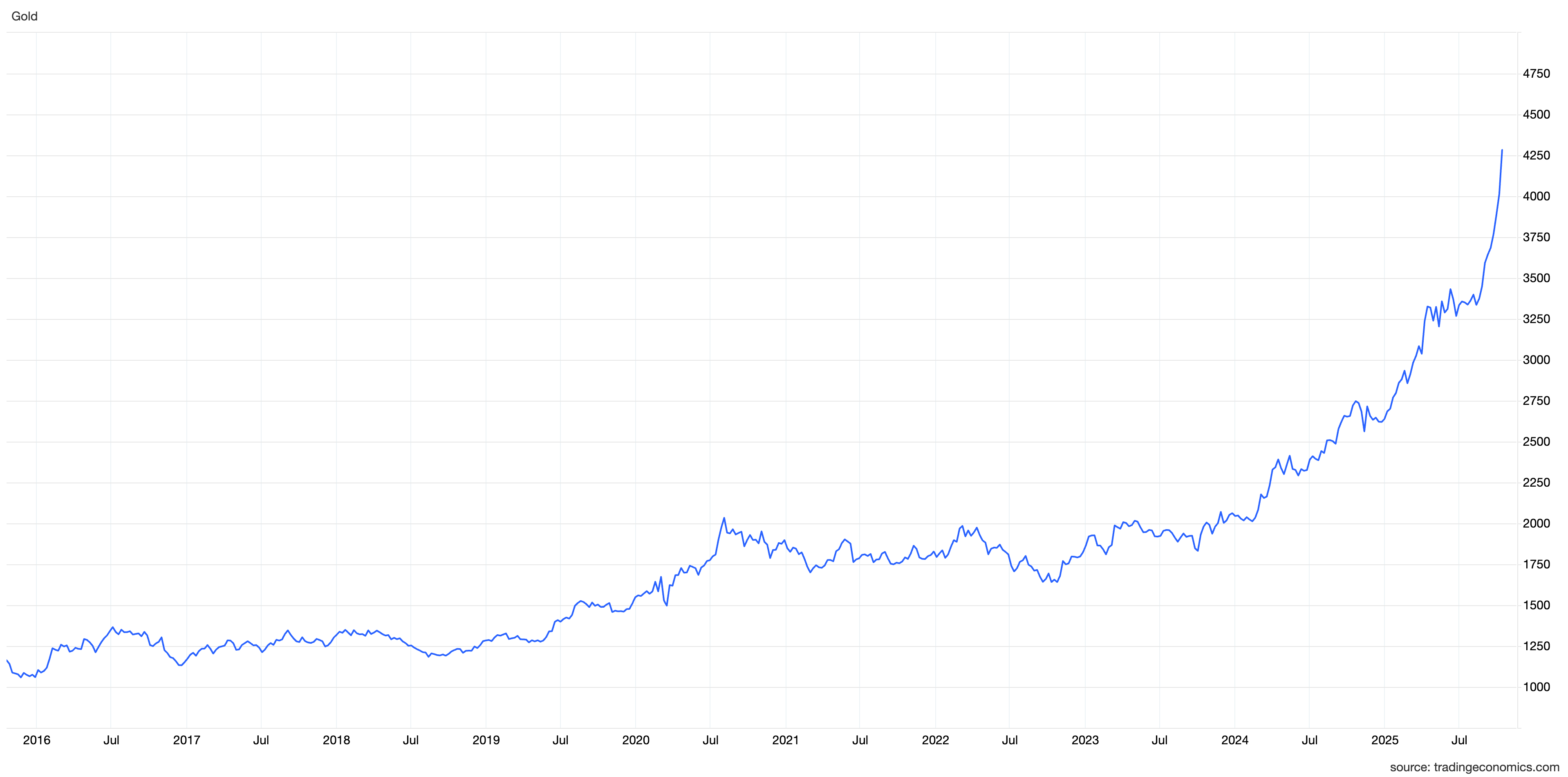

From July 22 to August 8, 2011, the S&P 500 index plummeted by 17%, a typical risk-off event. Counterintuitively, the US Treasury market, the very subject of the downgrade, received a massive inflow of safe-haven capital. Investors flocked to the Treasury market for shelter, causing the 10-year Treasury yield to drop sharply from around 3.00% in early July to near 2.00% by the end of August, with bond prices rising significantly. This demonstrated that in a global panic, US Treasuries were still the most liquid and relatively safest asset—the so-called "cleanest dirty shirt." At the same time, gold's performance was the most striking. The price of gold soared from around $1,620/oz in early August to a new all-time high of over $1,900/oz by the end of the month, a stunning gain that far outpaced all other asset classes.

The 2011 crisis revealed a clear "hierarchy of safe-haven assets": when the market faces widespread macroeconomic risk, capital flows from risk assets like stocks to US Treasuries. However, when the core of the crisis strikes at the credit and governance capacity of the United States itself, a portion of capital seeking ultimate safety bypasses Treasuries and flows directly into gold. In this moment, gold acts not just as a hedge against market volatility, but as the ultimate insurance against the systemic risk of the reserve currency issuer. For those investors truly concerned about the root of the crisis (i.e., US political and fiscal risk), increasing holdings of US Treasuries is not the solution. They seek a non-sovereign, apolitical, counterparty-risk-free haven—gold. Thus, the events of 2011 eloquently demonstrated that gold and Treasuries are not always substitutes. In a US credibility crisis, gold can become the ultimate safe haven, surpassing US Treasuries.

Modern Echoes and New Structural Drivers

If the events of 2011 were a preview, the market environment since 2022 marks a permanent structural shift. Subsequent downgrades by Fitch (2023) and Moody's (2025) reiterated the same concerns about US governance and fiscal issues as in 2011. However, a more profound trend has emerged since 2020: global central banks, particularly from emerging market economies led by China, India, and Turkey, have begun large-scale and sustained purchases of gold.

This trend accelerated significantly after the outbreak of the Russia-Ukraine conflict. The freezing of hundreds of billions of dollars of Russia's foreign exchange reserves by Western countries was a watershed event for global reserve managers. It demonstrated to the world, in an unprecedented way, the immense geopolitical counterparty risk associated with holding US dollars and US Treasuries. For any country with potential geopolitical friction with the United States, concentrating national wealth excessively in dollar-denominated assets is tantamount to placing its financial lifeline in the hands of others. This realization has given rise to a new class of gold buyers: strategic central bank reserves. Their purchasing behavior is not driven by speculation on short-term yields or price fluctuations, but by the strategic need for geopolitical insurance and reserve asset diversification.

This class of buyers is relatively insensitive to real yields, and their continuous purchases provide a powerful, structural demand base for the gold market. This new source of demand helps explain why the traditional negative correlation between gold and real yields has frequently broken down in recent years.

The 2011 crisis was a brief shock that exposed the vulnerability of the dollar system. The 2022 freezing of Russian assets was a clear demonstration of this vulnerability being exploited. "De facto default" is no longer just a sporadic crisis event; it has evolved into a constant background feature of the geopolitical landscape, driving a long-term and structural reallocation of global reserve assets from the US dollar to gold.

The Institutional Rise of Bitcoin: From Niche Asset to "Digital Gold"

In discussing the capital spillover caused by the "de facto default" of US Treasuries, the role of Bitcoin is becoming increasingly prominent. It is not just a synonym for cryptocurrency but an emerging macro asset with unique properties. To understand Bitcoin's strategic position in the current financial landscape, it is crucial to analyze its core asset attributes. It is these attributes, especially the striking commonalities with gold, that are the fundamental reason why the market has dubbed it "Digital Gold."

Absolute scarcity is the most fundamental commonality between Bitcoin and gold. Bitcoin's total supply is permanently locked at 21 million coins by its underlying protocol and can never be increased. This stands in stark contrast to fiat currencies, which can be printed infinitely by central banks. Gold's scarcity stems from physical limitations in the Earth's crust and the difficulty of mining, whereas Bitcoin achieves absolute scarcity through mathematical algorithms. Its supply growth path is completely transparent and predictable, with its production halving every four years, continuously slowing its supply growth rate. From an economic perspective, the Proof-of-Work (PoW) mechanism endows Bitcoin with a production cost. It transforms two inputs, computing power and electricity, into an abstract form of "digital labor." It is this process of continuously consuming real-world resources to "mint" new coins that gives its value a solid cost basis.

Bitcoin's architecture fundamentally subverts financial control. Its network is not owned or operated by a single entity but is maintained by a global, voluntary coalition of tens of thousands of independent nodes. This distributed structure eliminates the possibility of unilateral control by central authorities (like governments or banks), making actions such as freezing accounts, confiscating funds, or censoring transactions technically infeasible. It is this "trustless" characteristic, which requires trust only in mathematics and code rather than intermediaries, that shapes Bitcoin into a truly sovereign and independent asset. It exists outside the traditional financial and political systems, providing an ultimate safe haven for wealth.

At the same time, Bitcoin retains the scarcity of gold while completely shedding its physical constraints. Its divisibility, transferability, and portability allow it to be finely divided to suit any transaction size and to compress immense wealth into intangible digital information, enabling near-zero-cost, instantaneous global transfers via the internet. This extreme portability and liquidity represent a fundamental advantage that physical gold cannot match.

Both are ideal tools for combating fiat currency debasement and inflation due to their limited and difficult-to-create supply. When people lose confidence in the long-term purchasing power of their national currency, they naturally turn to these "hard assets" whose supply cannot be arbitrarily manipulated by policy. Gold and Bitcoin are not liabilities of any nation; their value does not depend on the credit guarantee of any government. This allows them to act as "safe havens" that transcend national credit during sovereign debt crises or heightened geopolitical risk. When a "risk-free" asset like the US Treasury begins to show credit cracks, this value, independent of any single credit system, becomes particularly precious. Like gold, Bitcoin itself does not generate interest or cash flow. Therefore, the logic for holding it is similarly influenced by the real interest rate environment. In a negative real yield context, the opportunity cost of holding non-yielding assets disappears, and their appeal as pure stores of value rises significantly.

Quantifying Bitcoin's Risk Profile

From a risk-adjusted return perspective, Bitcoin's high risk has historically compensated its investors accordingly. Data shows that from 2020 to early 2024, Bitcoin's Sharpe Ratio was 0.96, outperforming the S&P 500's 0.65 during the same period. More notably, its Sortino Ratio was as high as 1.86. This indicator, which only considers downside volatility risk, provides strong evidence that the vast majority of Bitcoin's volatility occurs in the upward price direction, known as "upside volatility."

The launch of spot ETFs has not only provided an investment channel but has itself evolved into a feedback loop that amplifies demand, becoming a core engine of price discovery. Academic research clearly indicates that ETF net inflows are a strong positive predictor of Bitcoin's price, with an explanatory power (R-squared) as high as 95%. Further statistical analysis using Granger causality tests confirms that ETF flow data leads Bitcoin's price movements in time and helps predict its future trajectory.

The "Currency Debasement Trade": A Grand Narrative Unifying Different Assets

Although gold and Bitcoin have distinctly different risk profiles, they both attracted significant capital in 2024-2025, driven by a powerful and unifying macro narrative: the "Currency Debasement Trade." This trading framework provides the core logical basis for understanding the capital rotation between these two assets. The core logic of the "Currency Debasement Trade" is that investors are losing confidence in the long-term purchasing power of fiat currencies against a backdrop of structural challenges facing major global economies, thus seeking assets that can hedge against this risk.